How to dodge taxes like a billionaire: Heartbeat trading

How accountants save the rich trillions when no one is looking.

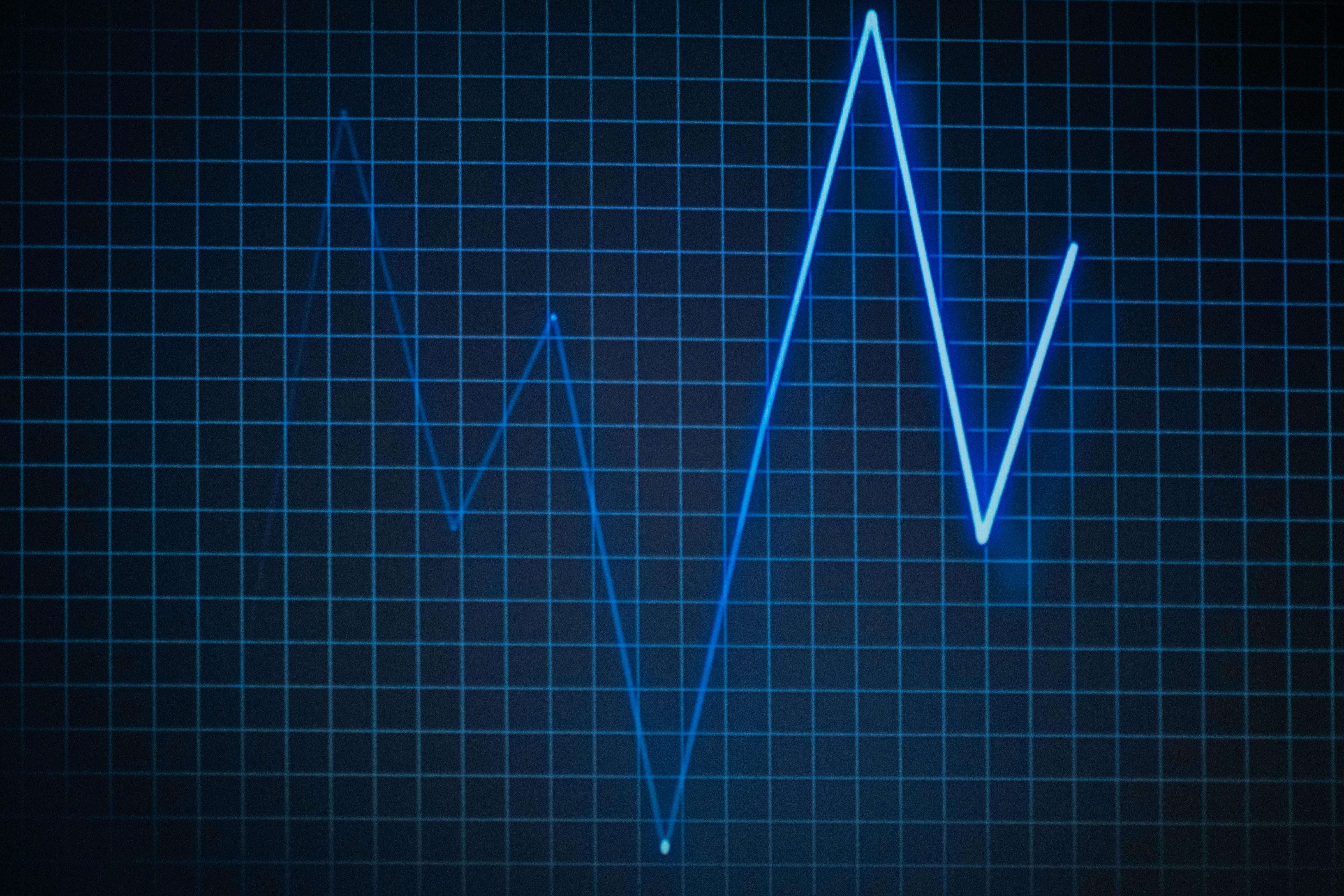

Imagine a heartbeat on a computer monitor. There is a flat line, interrupted by a sharp rise and equally sharp fall denoting the beat.

Occasionally, there will be a flat line for longer than normal and the doctors all panic. One doctor injects the patient with something that all the other doctors disagree with, and after a suitably tense pause, the heartbeats come back.

I will admit I get all my medical knowledge from reruns of House.

But there is one other place where you get this heartbeat image: Financial graphs of Exchange Traded Funds (EFT).

An ETF is a type of index fund that has garnered massive popularity over the last decade, with more than $8 trillion held in ETFs in 2023, for two major reasons.

Partly because the yearly fees on an ETF are far lower than an actively managed fund, but mostly because it is considered more ‘Tax Efficient’.

If, like me, you have never heard this expression before, you might be forgiven for thinking that tax efficiency means being able to do your taxes… efficiently. Maybe ETF’s come with a form you can hand your accountant and get all your tax returns sorted in a lunch break.

But tax efficiency is just another name for holding off paying taxes for years, if not decades. The only difference between tax efficiency and tax dodging is that theoretically, sometime in the far future when you sell all your share of the index fund, you will have to pay all the taxes that you owed. Yes, the government eventually gets their money, but you try not paying your income taxes for 40 years and see how far that gets you.

Let’s start at the beginning:

Index funds, like mutual funds and ETFs, hold a basket of shares on your behalf. The idea for this is simple: you’re an idiot.

If I asked you to guess which shares would be valuable 30 years from now, you’re gonna be wrong. If you were any good at guessing the future, you’d be making millions guessing lotto numbers and would never have bought skinny jeans.

Instead, by owning the whole basket of shares, you assume that some will fail, and some will succeed. On average, the good outweighs the bad, and you profit from the difference.

There are lots of different baskets of shares that you can pick, but the most common is the S&P 500. It’s the top 500 most valuable companies in America.

All the ETF does is buy shares of these top 500 companies, selling the shares of companies are no longer considered top 500, and adding in the new up-and-comers. It’s so basic that even a computer can do it…which they do and why the fees are so cheap.

Usually, when you sell a share, you are taxed on whatever profit you made. If you sell a share for $10 profit, you might have to pay around $2 in taxes to the government. If that doesn’t sound like such a big deal, add ten or eleven zeros to each number.

How do you dodge paying these huge taxes? One method is called a Heartbeat trade.

You only pay taxes when you sell a share. Just holding onto it does nothing. You also don’t pay taxes when you trade shares for other shares.

So, imagine you’re in charge of an ETF, and the computer buzzes, telling you its time to sell all your shares of ‘Genuine Parts Company’….

Ok I double checked and that is currently a legitimate company on the S&P500. But my lord does it sound like a drug front that even the writers of NCIS:Miami wouldn’t have created…

So, the computer tells you it’s time to sell all your shares of ‘Genuine Parts Company’ and start buying shares of Tesla.

I turn to my local investment banker friend, that I know already owns Tesla shares. Rather than purchasing them with money, I offer to trade with him a few million shares of my ETF in exchange for a few million shares of Tesla.

No money changed hands, so there is no tax.

The very next day, I offer to buy back my ETF shares, and offer him shares of Genuine Parts Company.

No money changed hands, so there is no tax.

On a graph it looks like a massive spike one day, and massive drop the next, on an otherwise steady line. Hence the name.

Because we went through this charade, I end up with the shares I need, but without ever having to pay the taxes. The investment banker usually owns the company that owns my ETF fund, so all of this just looks like an accounting trick to balance the books.

Eventually, when I am old and grey and need to sell my shares to pay settlement on my 4th divorce, I would be expected to pay the taxes I owe. But there are 3 factors that make this waaaaay better than the alternative.

1. Compound Interest.

I’m not here to explain math to you; My high school math teacher knows that I’m not qualified for anything harder than long division… but the money that should have been taxed is reinvested, leading to more money that should be taxed and instead is reinvested, leading to more money…. Effectively, this ‘tax efficient’ method is the equivalent of getting a loan from the government and paying 0% interest on it. When is the last time you got a 0% interest loan?

2. Tax rates.

The American Capital Gains Tax for individuals selling their shares was 28% in 1987. Today its 20%. By paying now rather than back when it was owed, I save more than a quarter of the taxes. Its not a dodge, because everything is totally legal, but its still a massive saving.

3. Why sell?

One of the basic ways to minimize your taxes as a rich person, is to buy everything with debt. You don’t use a credit card, because paying overdue payments and high interest is for the poors, but rather you use a bank loan, with your assets held in collateral. ETF shares are considered assets, and if you ask a bank for a $100 million dollar loan with $120 million dollars of ETF shares, the bank will be more than happy to oblige. You probably won’t have to wait in line or anything.

You don’t pay taxes on debts, which means, so long as you never sell the shares, you never pay the taxes. The game plan of the ultra-rich is to rack up massive debts and die. You might have to pay the 5 or 6% interest on the bank loan, but that’s still much better than the 20% taxes you’d otherwise be charged.

Heartbeat trades are not new. Every ETF uses them, and chances are your pension or superannuation partially benefits from their existence. This isn’t the work of a mustachioed villain, cackling in the dungeon of a mansion, as lightning strikes in the background… it’s an accounting practice handled by people whose idea of ‘Casual Friday’ is probably wearing a non-grey tie.

But, like most of the obscure aspects of finance, it slowly siphons money from the government and the average worker and gives it to the already rich. When governments cry that they can’t afford to fund nurses, or need to close the local school, it’s things like this that exacerbate the financial pressure.

Or, who knows. Maybe you should just work harder. Sounds like a reasonable argument.